Last Mile Credit Linkage to Strengthen Rural Livelihood

by Arkajyoti Patra

9th June, 2021

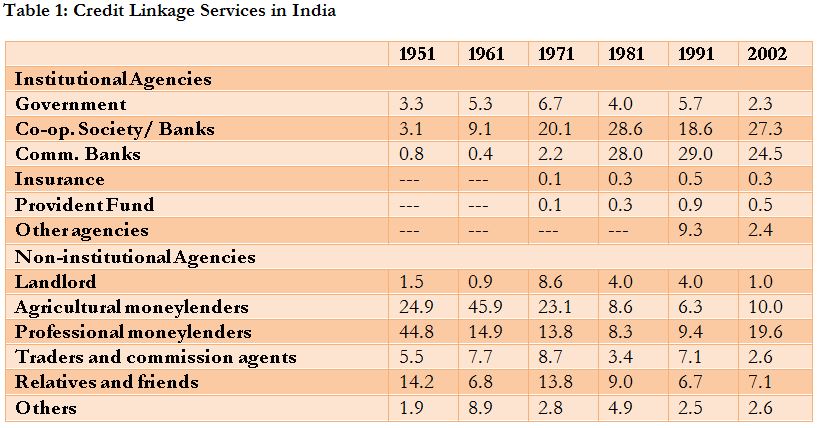

Rural credit markets in India comprise of both formal and informal channels. Though the market is fragmented, many approach informal channels for their credit requirements. The most common source of credit in the villages of Koraput&Nabarangpur is from moneylenders, aka Sahukaars. These moneylenders charge around 60% to 120% interest annually. Although the share of informal credit has dropped drastically, it still accounts to almost half of all credit linkage services in the country as shown in Table 1 below;

Rural credit markets in India comprise of both formal and informal channels. Though the market is fragmented, many approach informal channels for their credit requirements. The most common source of credit in the villages of Koraput&Nabarangpur is from moneylenders, aka Sahukaars. These moneylenders charge around 60% to 120% interest annually. Although the share of informal credit has dropped drastically, it still accounts to almost half of all credit linkage services in the country as shown in Table 1 below;

Case of Sabita Jena

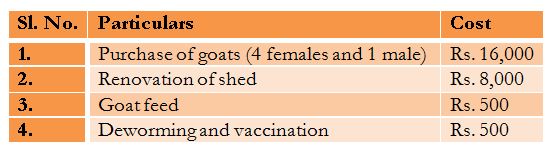

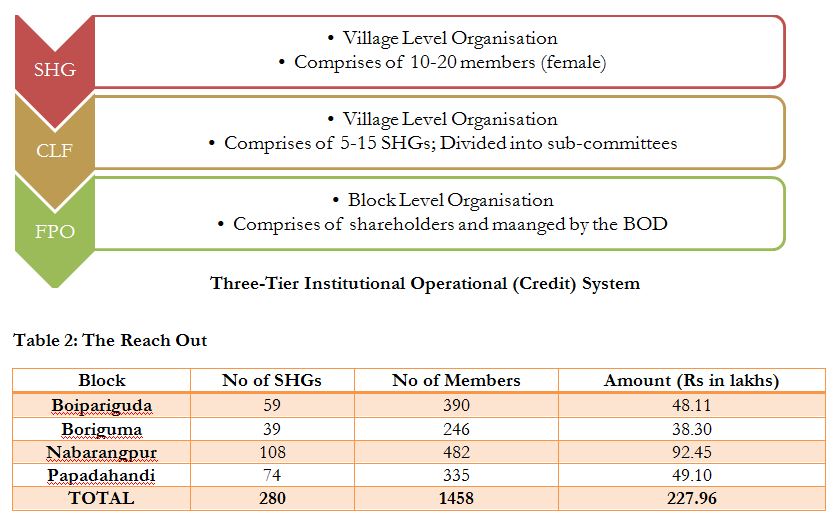

Patneswari Agricultural Producer Co. Ltd. (PAPCL) with support from Harsha Trust partnered with Rangde to give credit access to its shareholders for agriculture and livestock rearing and/or other business activities. Sabita Jena is one such twenty-four year old beneficiary who lives with her mother in the village of R. Maliguda. Abandoned by her father, she is the sole earning member in the family. She works as a Community Resource Person in some government and non-government organizations to make ends meet. Though the family is also involved in agriculture and livestock rearing as well but due to lack of timely credit at a reasonable interest rate they refrained from investing into them beyond their available financial means. When PAPCL approached the shareholders from R. Maliguda to provide credit linkage, only three were selected by Rangde based on their credit history, Sabita being one of them. She applied for a loan of Rs. 20,000 for goat rearing. The estimated cost division for the same is shown in Table 2 below.